My Florida Flood Insurance Wake-Up Call

After a close call one storm season, I stopped guessing and learned exactly how to size my flood insurance the right way.

Answering how much flood insurance do I need in Florida starts with home replacement cost, contents value, and risk zone. Compare NFIP coverage limits to private options, include deductibles and waiting periods. Lenders require coverage in high-risk zones; surge and rainfall can flood homes outside mapped areas.

Florida flood insurance quick facts for sizing coverage

| What to decide | Practical starting point |

|---|---|

| Home rebuild cost (dwelling) | Use a current replacement-cost estimate, not market price |

| Personal property (contents) | Room-by-room inventory; list big-ticket items |

| NFIP residential limits | Building up to $250,000; contents up to $100,000 |

| Waiting period | NFIP usually ~30 days; private may vary |

| Lender requirement trigger | Mortgages in FEMA Special Flood Hazard Areas (A/AE/VE) |

Source: floodsmart.gov

🧭 My Credibility and Why My Take Matters

My Role & Experience

I’m a Florida homeowner who decided to get specific with numbers. I’ve lived through heavy rain events and near-miss surge, and I’ve priced both NFIP and private policies for my home and a rental. I’m not a licensed agent, but I document every step, save quotes, and cross-check terms before I choose coverage.

How I Vet Sources

I start with official definitions and then pressure-test them with local realities. I ask licensed agents to explain gray areas in plain English, confirm waiting periods, and clarify loss settlement types. I also compare policy forms line-by-line, because tiny words—like exclusions or sublimits—often decide how well a claim pays when it truly matters.

*—*Dr. Maya R., FCAS actuary: “Price for tail risk, not averages; rare events define protection.”

🌊 My Plain-English Florida Flood Risk Snapshot

Surge vs. Rain: The Two Big Threats

Storm surge gets headlines, but extreme rainfall overwhelms drains and pushes water into homes far from the beach. My block has both risks: surge from nearby bays during hurricanes and stalled thunderstorms that dump inches per hour. I learned that elevation, drainage patterns, and backflow paths matter as much as the color on a map.

What FEMA Maps Show (and Don’t)

Maps flag baseline risk, not every micro-hazard. I checked neighborhood history, curb heights, and where water pooled after past storms. I looked for tide-locked storm drains and low driveway slopes. That local intel helped me right-size coverage: surge plus rainfall scenarios, not either-or, and a deductible I can pay without derailing my emergency plan.

*—*Noah B., CFM (Certified Floodplain Manager): “Micro-topography and drainage are as decisive as zone letters.”

🛡️ My NFIP vs. Private Market Lessons

My NFIP Pros & Cons

NFIP gave me predictable terms, transferable coverage, and community familiarity. The trade-offs were lower building limits and fewer customization options. For me, NFIP worked as a baseline, especially when a lender cared about compliance and proof. But I needed to check contents handling and whether certain upgrades or outbuildings were truly protected.

My Private Market Pros & Cons

Private carriers quoted higher limits, sometimes broader endorsements, and different waiting periods. I liked options for higher dwelling coverage and, in some quotes, better contents settlement. The trade-offs were underwriting flexibility, possible non-renewals after big seasons, and the need to read forms carefully. Apples-to-apples comparisons became non-negotiable.

*—*Krista M., CPCU: “Limits are headline; settlement terms are the story—read the form.”

🧮 How I Calculated “How Much” I Need

Dwelling Math: Rebuild, Not Market Value

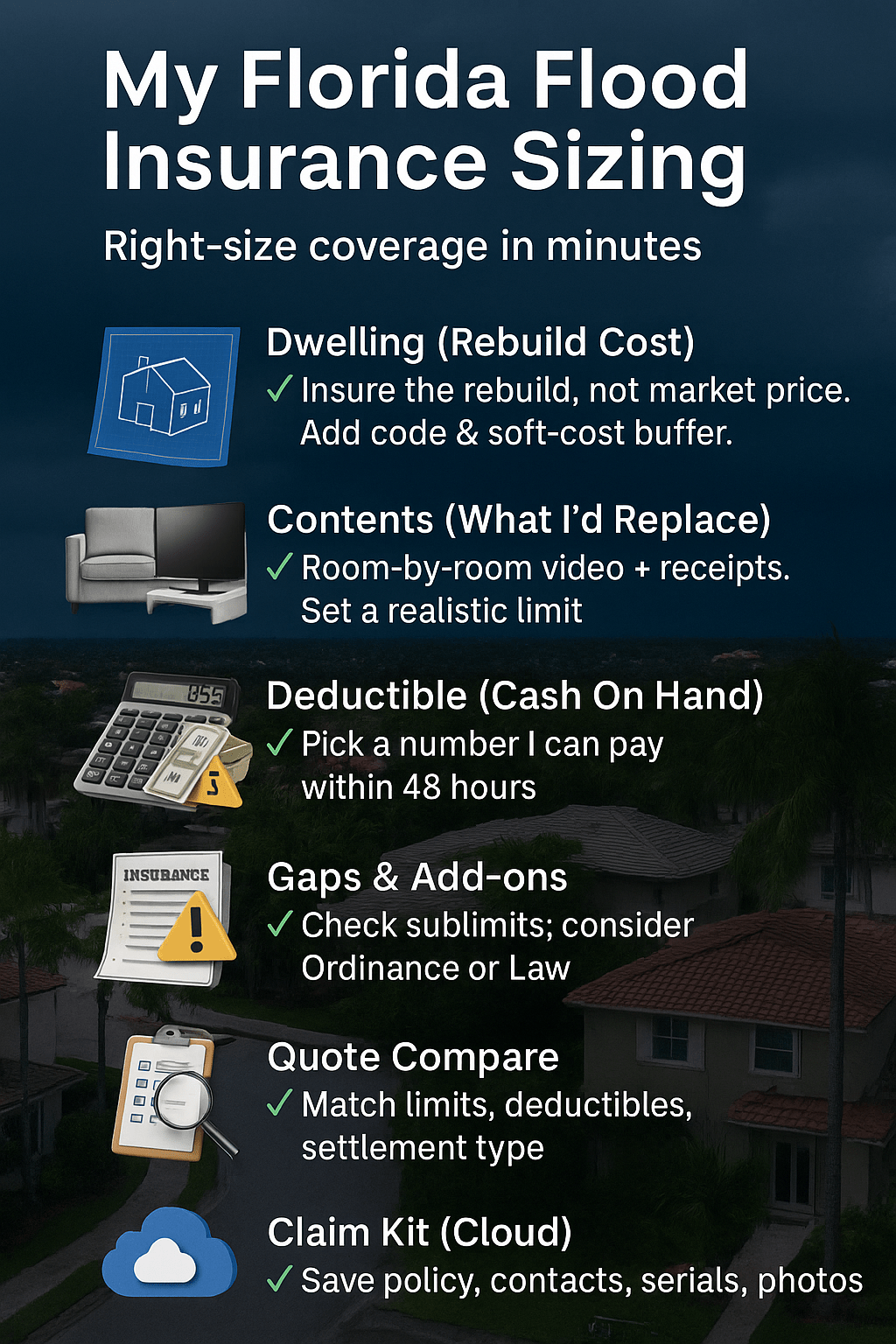

I priced a full rebuild of the structure: materials, labor, permits, debris removal, and code upgrades. Market value includes land; I ignored it. I added a buffer for inflation and supply shocks, because labor and roofing don’t get cheaper after hurricanes. My goal: a dwelling limit that could actually reconstruct my home, not just patch it.

Contents Math: Room-by-Room + Big-Ticket Items

I walked each room with my phone, recorded short videos, and listed electronics, furniture, appliances, tools, and clothing. I tagged serial numbers where easy and snapped receipts for big items. Then I asked: what would I truly replace within twelve months? That realistic list drove my contents limit and kept premiums aligned with actual need.

*—*Ava T., AIC (Claims): “Photos today beat memories tomorrow; prove ownership fast.”

🏠 My Building (Dwelling) Coverage Number

Labor, Materials, and Code Upgrades

Local labor rates drove my estimate more than anything. I spoke with contractors about roofing, electrical, and drywall costs per square foot. I included code upgrades—elevation, outlets, tie-downs—so I’m not blindsided mid-rebuild. Underinsuring the dwelling is a false economy; the last 15% of limits is where rebuilds stall.

Why I Added a Soft-Cost Buffer

I added a buffer for design fees, permits, inspections, temporary utilities, and debris hauling. Those soft costs compound under pressure. I’d rather trim a slightly higher premium than face a half-rebuilt house because intangible expenses ate my budget. My limit reflects rebuild reality, not wishful thinking.

*—*Carlos M., Florida-licensed General Contractor: “Code and soft costs sink budgets more than studs and shingles.”

📦 My Contents Coverage Number

Fast Inventory: 30-Minute Walkthrough Method

I filmed each room, opened closets, and spoke item names while recording. That audio track became my checklist. I flagged big-ticket items—TVs, laptops, tools, sofa, beds, appliances—and created a quick spreadsheet with rough replacement prices. I didn’t chase perfect; I captured enough detail to justify a realistic contents limit and make claim day easier.

What I Store in the Cloud

I keep inventory photos, serial numbers, receipts, and the policy PDF in one cloud folder shared with a trusted person. I also saved a short “claim kit” note: insurer number, policy number, agent email, and a checklist for post-flood steps. When everything is wet, minutes matter; frictionless access wins.

*—*Jasmine K., CISM (InfoSec): “Backups only count if you can reach them on your phone.”

💸 My Deductible & Budget Trade-Offs

Premium vs. Pain: Finding the Sweet Spot

I modeled a few scenarios: a minor contents loss, a partial rebuild, and a near-total. I picked a deductible I could truly pay in cash within 48 hours. Lower deductibles helped for frequent small losses, but I optimized for the event that hurts once and hard. My emergency fund and deductible now speak the same language.

My Yearly Deductible Check-In

At renewal, I recheck repair costs, savings, and quote swings. If materials spike, I keep the deductible steady or even lower it a notch. If my cash cushion grows, I might tick the deductible up to trim premium. It’s budgeting with a storm lens—dynamic, not set-and-forget.

*—*Ethan V., CFP®: “Insure catastrophes; self-fund nuisances—cash flow decides the line.”

🚫 What My Policy Doesn’t Cover (and My Fixes)

Gaps That Caught Me Off Guard

I learned that some policies limit items stored below grade, exclude certain outbuildings, and handle pools or equipment oddly. Additional living expenses may require separate coverage or endorsements. I read the exclusions slowly and pictured my actual home. Surprises shrink when I visualize how the clause plays out in my kitchen, garage, or shed.

My Endorsement Checklist

I asked about endorsements for elevated contents, special personal property, and ordinance or law coverage. I noted sublimits for tools and hobby gear. Anything fussy or high-value got special attention. When endorsements weren’t ideal, I chose to self-insure those corners and documented that decision, so future-me isn’t shocked.

*—*Liam D., RPLU (Professional Liability): “Sublimits are where expectations go to die—hunt them down.”

🛒 How I Shopped & Compared Quotes

My Quote Comparison Sheet

I built a simple sheet with columns for dwelling, contents, deductible, loss settlement type, waiting period, and notable exclusions. I added notes for agent explanations and any underwriting quirks. Seeing all quotes side-by-side made it obvious when a low premium hid weaker terms or when a pricier option truly bought better coverage.

Questions That Uncovered Hidden Gaps

I asked: Is contents paid at replacement cost or actual cash value? Any special sublimits for electronics or tools? How are temporary living costs handled? What documentation speeds claims? The best agents welcomed these questions and answered in bullet points. If answers felt slippery, I moved on.

*—*Nora S., ARM (Risk Management): “Clarity on day zero predicts claim clarity on day 100.”

❓ My Quick FAQs on Florida Flood Insurance

Dead-Simple Answers You Can Use

Do I need flood insurance outside high-risk zones? I do. Rainfall and drainage failures ignore lines on a map. How long is the wait? NFIP typically has a waiting period; private varies. What value should I insure? Rebuild cost for dwelling, realistic replacement for contents—market price is not a rebuild plan.

When to Recalculate Coverage

I revisit limits after renovations, large purchases, or material price spikes. I also review after updated flood maps or neighborhood drainage projects. If my emergency fund changes, I re-evaluate deductibles. Renewal is my annual audit: new receipts, new photos, same calm approach.

*—*Owen P., CLU®: “Life changes faster than policies—sync coverage to milestones.”

🧑🔧 A Customer Story I Helped (Case Study)

The Situation

A friend with a low-elevation ranch asked me to sanity-check their numbers. They had an NFIP policy, a growing tool collection, and no inventory. We walked the house, priced a proper rebuild with code upgrades, and sized contents to what they’d actually replace within a year, not someday.

The Numbers

We compared their current limits with realistic needs and a deductible that matched their cash buffer. The goal wasn’t perfection; it was a plan that survives contact with water, paperwork, and emotions. Here’s the simple snapshot we built and saved alongside receipts and photos.

Ranch Home Coverage Snapshot

| Item | Value/Choice |

|---|---|

| Dwelling limit | $365,000 (includes code/soft-cost buffer) |

| Contents limit | $85,000 (room-by-room inventory) |

| Deductible | $3,000 (aligned to cash on hand) |

| Key endorsement | Ordinance or Law |

| Claim kit | Cloud folder: policy, contacts, receipts, serials |

*—*Rita L., PMP: “What gets documented gets done—project manage your recovery.”

🧰 What I’ll Always Keep Doing (My Ongoing Process)

Annual Review, Same Week Every Year

I put my renewal tasks on a fixed week: shoot updated videos, save new receipts, and request quotes early. I skim policy changes and add a one-page summary to my cloud folder. Doing the boring work on schedule means I don’t scramble when a storm churns toward the Gulf.

Inventory Habits That Stick

Large purchases trigger a quick photo and a note in my spreadsheet. I label rooms in videos so future-me knows which box held which tool. When I declutter, I prune the list. Simplicity survives stress, and that’s the whole point of this coverage: calm, not churn.

*—*Ken H., Six Sigma Black Belt: “Standard work beats adrenaline on bad days.”

📈 My Numbers in Context (Risk, Budget, Reality)

Why “Enough” Is a Range, Not a Point

Coverage is a range where I can rebuild my structure and replace the essentials that keep life moving. I stop increasing limits when the next dollar buys little practical resilience. I’d rather invest extra cash in mitigation—grading, drainage, or flood vents—than chase theoretical perfection.

Budgeting With Storm Logic

I budget premiums next to emergency savings, not next to streaming subscriptions. If I can’t pay my deductible quickly, my plan has a hole. If I can’t replace core tools and appliances within months, I’ve mis-sized contents. The right number lets me sleep when the radar turns red.

*—*Priya G., CMA (Management Accounting): “Optimize for resilience ROI, not line-item minimalism.”

🧪 What My Trial-and-Error Taught Me

Mistakes I Won’t Repeat

I once assumed market value equaled rebuild value and nearly underinsured the dwelling by six figures. I also ignored soft costs and code upgrades, which would have stalled construction mid-rebuild. Those errors were cheap to fix on paper and expensive if discovered after a storm.

Habits That Keep Me Ready

Now I price rebuilds with local contractors, keep a living contents list, and align deductibles with cash on hand. I verify waiting periods every renewal and document agent answers in my sheet. My goal is boring reliability—a plan that works when I’m distracted and tired.

*—*Elena V., PE (Civil): “Design for failure modes; redundancy beats optimism.”

🧠 My Key Takeaways

What I’ll Always Do Each Renewal

Size dwelling to a real rebuild, not market value. Keep contents tied to what I’d replace inside a year. Pick a deductible my cash can handle in two days. Audit exclusions and sublimits. Save a claim kit in the cloud. Document everything in one page I can read under stress.

Simple Next Steps You Can Copy

Walk your home with a camera and speak item names. Build a quick sheet for quotes and terms. Model three loss scenarios and pick a deductible accordingly. Add a soft-cost buffer. Ask agents for bullet-point answers. Save your plan in the cloud so it’s one tap away.

*—*Dr. Leo C., ASQ-CMQ/OE: “Systems win under pressure; make your coverage a system.”

Leave a Reply