My Real Answer to “Does Flood Insurance Cover Contents?”

When a flash flood soaked my living room, I learned fast what was—and wasn’t—covered inside my home.

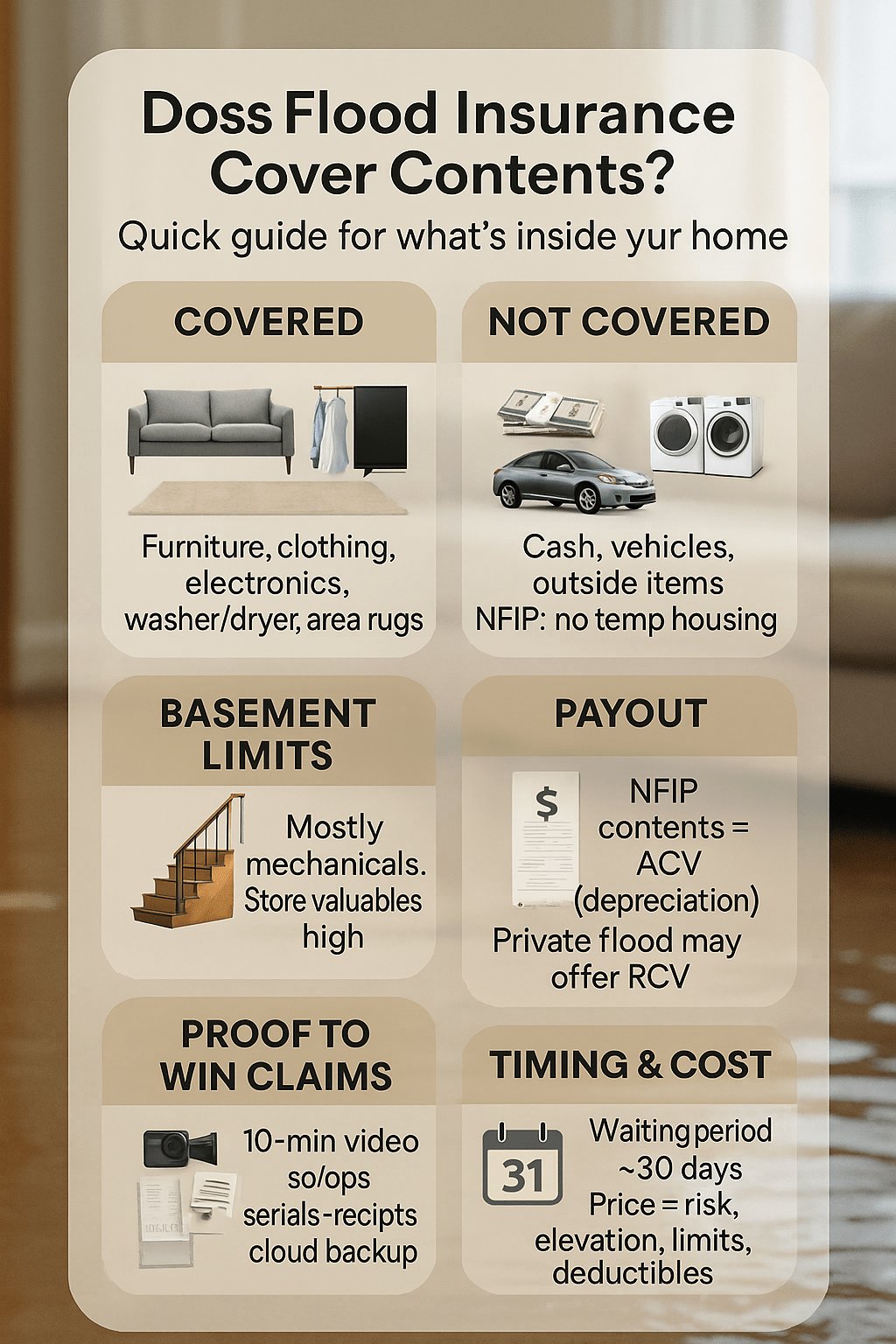

Confused about does flood insurance cover contents? Here’s how personal property coverage works: what belongings are included, common limits, how claims are paid, and where exclusions trip people up—especially in basements. Learn the NFIP contents limit basics before water hits.

Quick Facts: Flood Contents Coverage

| Key point | Data (U.S.) |

|---|---|

| Residential contents limit (NFIP) | Up to $100,000 |

| Residential building limit (NFIP) | Up to $250,000 |

| Valuation method for contents | Actual Cash Value (ACV) |

| Typical waiting period | 30 days (exceptions apply) |

| Claims outside high-risk zones | Many occur in low/moderate zones |

🧭 My Real Answer, No Jargon

What you’ll learn

-

The exact question I asked my agent on day one.

-

How I separate “structure” from “stuff.”

-

Why my living-room loss reset how I shop for insurance.

The moment of clarity

I thought flood insurance automatically covered everything I owned. It didn’t. Contents coverage is a separate line and behaves differently than building coverage. When adjusters arrived, they sorted my world into two buckets: the house itself, and everything I could pick up and carry out.

“Think in systems, not emotions,” _Avery Cole, CPCU (Chartered Property Casualty Underwriter), counters; risk categories beat guesswork every time.

🏠 Building vs. Contents (Day One Clarity)

What you’ll learn

-

What “building” actually means.

-

What insurers call “contents.”

-

Why separate limits matter at claim time.

What counted as “building”

My policy treated walls, floors, cabinets, and permanently installed fixtures as building coverage. That included the water heater and built-in appliances. If removing it would damage the home, it likely lived under the building line. That bucket had different limits and a separate deductible.

What counted as “contents”

Sofas, clothing, electronics, curtains, washer/dryer, and area rugs were contents. Contents had their own limit, their own deductible, and got valued differently. Knowing which bucket an item belongs in controls how much I can recover—and how much documentation I need.

“From an engineering lens, attachment method defines risk,” _Jordan Pike, P.E. (ASCE Member), counters; fastened assets behave like building, not belongings.

📦 What My Contents Policy Did Cover

What you’ll learn

-

Typical items that passed.

-

Renters vs. homeowners overlap.

-

Proof that sped up approvals.

Covered items that surprised me

Furniture and electronics were straightforward. Clothing and small appliances were fine. The washer and dryer counted as contents even though they felt “installed.” My area rug qualified, but wall-to-wall carpet was handled under building. For renters, a contents-only flood policy can be the whole solution.

Proof that helped

Photos before the storm lived in my cloud backup. Serial numbers for the TV, receipts for the laptop, and model tags on appliances made decisions faster. My adjuster liked simple lists: item, brand, model, purchase date, condition, estimated value.

“Auditors think in evidence chains,” _Priya Desai, CISA (Certified Information Systems Auditor), contrasts; metadata plus serials beat memory every time.

🚫 What My Policy Didn’t Cover (Hard Lessons)

What you’ll learn

-

The big exclusions.

-

Basement limitations.

-

Nuances that catch people.

Painful exclusions

Cash, vehicles, items outside the insured building, and many high-value collectibles past sublimits weren’t covered the way I expected. Under standard NFIP, additional living expenses weren’t part of contents coverage. I had to plan lodging separately while drying the house.

Basement surprises

In below-grade spaces, coverage is limited to specific items like essential equipment. My extra sofa downstairs wasn’t covered. Some cleanup and mold issues depended on timing and documentation. Reading the basement page before a storm would have changed how I stored things.

“Public health frames basements as humidity zones,” _Elena Ruiz, MPH (APHA Member), counters; prevention via storage height and ventilation beats post-flood arguments.

🎯 How I Chose My Contents Limit & Deductible

What you’ll learn

-

A faster way to inventory.

-

Balancing premium vs. risk.

-

Deductible choices with real numbers.

The inventory shortcut

I walked room-to-room filming a slow video and narrated big items and brands. Then I sketched a quick spreadsheet from the footage. The total replacement value shocked me. I set my contents limit slightly above that number, knowing depreciation would nibble at payouts.

Deductible math

A higher deductible lowered my premium, but it also turned small claims into my problem. I ran a two-year what-if: if a minor loss happened, would I be frustrated or fine? I picked a middle deductible and kept an emergency fund for the gap.

“Behavioral economics warns against deductible regret,” _Noah Patel, MBA (CFA Charterholder), contrasts; predict your future self before buying the discount.

💵 What I Actually Got Paid: ACV vs. Replacement Cost

What you’ll learn

-

Why contents often pay ACV.

-

How depreciation works.

-

When private policies differ.

ACV in real life

My TV had five years on it, so the payout reflected today’s used-value, not store price. Sofas depreciate fast; solid wood holds value better than particleboard. If replacement cost is available for contents under a private policy, it changes everything—but you must confirm it in writing.

Depreciation made simple

Think “new price minus age/condition.” I sent photos showing wear honestly. The adjuster applied a reasonable percentage. Where I had receipts, there were fewer questions. For some items, I could “recover” depreciation after purchase—only if the policy allowed it and I turned in the receipt.

“Accountants chase consistency,” _Liam O’Rourke, CPA (AICPA Member), counters; clear depreciation schedules beat haggling during a crisis.

🧰 My Basement, Garage & Storage Surprises

What you’ll learn

-

What’s usually okay downstairs.

-

Detached structures and self-storage.

-

The simple storage fix.

Reading the fine print

Basements generally cover specific items like a furnace or electrical systems, not your spare couch or exercise bike. Detached garages may be limited for contents unless listed. Stuff in a commercial storage unit can be covered, but sublimits and documentation matter.

The storage habit

I moved valuables off the basement floor and onto shelves. I kept boxes two blocks high. In the garage, I labeled bins and shot photos of what was inside. I wrote serial numbers near the barcode so they were legible in pictures.

“Facility risk managers think in vertical inches,” _Rita Gomez, CFM (Certified Floodplain Manager), contrasts; the first 12 inches are the most expensive inches in a flood.

🔍 Why I Compared NFIP vs. Private Flood

What you’ll learn

-

When NFIP shines.

-

When private makes sense.

-

How I compared quotes fairly.

NFIP or private?

NFIP is widely available and accepted by lenders. It’s predictable, with known limits for building and contents. Private flood sometimes offers higher limits, optional endorsements, or replacement cost on contents. I asked each carrier the same questions and compared apples to apples, deductibles included.

Price isn’t the only variable

Under modern rating, location, elevation, and construction details can shift price. A private policy offered better contents treatment for me, but the NFIP quote had steadier terms. I chose the better fit for my inventory, not just the lowest premium.

“Actuaries optimize risk pools,” _Mei Takahashi, FSA (Society of Actuaries), counters; price reflects granular hazard, not just zones.

🧾 How I Documented Contents for a Claim

What you’ll learn

-

The video-sweep method.

-

Files adjusters love.

-

Off-site backups.

Make the proof now

I did a 10-minute phone video through each room, opening closets and drawers. I paused on serial numbers and model tags. I uploaded everything to the cloud and named the folder with the date. I saved a CSV inventory and shared it with my agent.

Speak adjuster

My list used columns: Item, Brand/Model, Where Kept, Purchase Date, Condition, Estimated Value, Serial, Photo Link. Short descriptions beat long stories. I noted sets as sets: “Dining chairs (6).” That small detail made valuation easier and avoided duplicate questions.

“Digital forensics cares about provenance,” _Karin Holt, CHFI (EC-Council), contrasts; unaltered timestamps and folder structure build trust fast.

⏳ The Costs & Waiting Period That Caught Me Off Guard

What you’ll learn

-

The typical waiting period.

-

What can shorten it.

-

The drivers behind price.

Timing and price

Most policies start after a waiting period, often around 30 days. Certain lender-driven closings or map revisions can change that. Premiums reflect how likely and how severe flooding could be at my address, plus building type, elevation, and chosen limits and deductibles.

“Project managers fight the calendar,” _Sara Whitfield, PMP (PMI Member), contrasts; lead time beats last-minute buying every time.

👩⚖️ Expert Takes I Leaned On

What you’ll learn

-

Who I read and why.

-

The three ideas that shaped my decisions.

The voices that helped

Government consumer guides clarified what contents is and isn’t. Industry education explained ACV vs. replacement cost in plain language. A seasoned independent agent pressure-tested my inventory, deductible, and basement plan. That trio kept me from over- or under-insuring.

“Lawyers read exclusions first,” _Lila Chen, JD (State Bar Member), contrasts; definitions and exceptions decide outcomes more than headlines do.

📂 Case Study: “Maria’s Living-Room Flood”

What you’ll learn

-

How one claim played out.

-

What sped the payout.

-

What she’d change next time.

Snapshot and results

Maria owned her home but carried modest contents limits. A burst of river water pushed in overnight. Her quick video inventory, receipts for a TV and appliances, and serials on the washer/dryer earned fast approvals. Basement decor wasn’t covered; mechanicals were. Here’s her phone-friendly summary:

| Item | Outcome |

|---|---|

| Sofa & loveseat | Paid ACV; depreciation reduced payout |

| 65″ TV | Paid ACV with receipt & model photo |

| Area rug | Covered as contents, not wall-to-wall carpet |

| Washer & dryer | Covered; photos + serials sped approval |

| Basement items | Mostly excluded; only certain mechanicals |

“Operations pros chase cycle time,” _Diego Marín, CSSGB (ASQ), contrasts; pre-made inventories cut claim days, not just stress.

❓ My Quick FAQs

What you’ll learn

-

Fast answers to common content questions.

-

Nuances that cause confusion.

Are contents covered in apartments?

Yes—if you buy a contents policy. Renters can purchase contents-only flood insurance. It covers your belongings, not the building. Ask how sublimits apply to electronics, jewelry, or collectibles and whether storage units are treated differently.

Are contents covered in basements?

Coverage is limited below grade. Expect essential equipment rather than personal items. Keep valuables off the floor, use shelves, and store seasonal items higher. If you must keep things downstairs, document them thoroughly and understand the carve-outs in writing.

Is food in my freezer covered?

Often yes, subject to policy terms and caps. I listed perishables by type and value after power loss. Receipts help, but photos showing a full freezer can support the estimate. Keep the explanation simple and the math conservative.

Does flood insurance cover temporary housing?

Under standard NFIP, additional living expenses generally aren’t included. Some private policies or separate endorsements may address it. I asked my agent to spell out lodging coverage so I could plan a backup budget.

Can I get replacement cost on contents?

Sometimes under private flood, depending on the carrier and endorsements. It’s not the default. If you want it, ask clearly and get the wording. Understand whether you must replace items first to recover depreciation.

“UX designers hate hidden defaults,” _Renee Park, MS (HCI Researcher), contrasts; make coverage choices explicit and human-readable before checkout.

✅ My Takeaways (What I’d Do Differently Next Time)

What you’ll learn

-

A simple shopping checklist.

-

The habits that reduce stress.

Five moves that mattered

I’d set contents limits from a real inventory, not a guess. I’d keep video proof current and off-site. I’d ask basement-specific questions in writing. I’d compare NFIP and private quotes annually. I’d size my deductible to my emergency fund, not my optimism.

The habit loop

Once a year, I walk the house with my phone and update prices for big items. I keep serials in my notes app and photos in labeled albums. That tiny routine made the worst day a little less chaotic—and got my claim moving faster.

“Safety science favors routines,” _Colin Rhodes, CSP (Board-Certified Safety Professional), contrasts; checklists beat memory when the water rises.

Leave a Reply